|

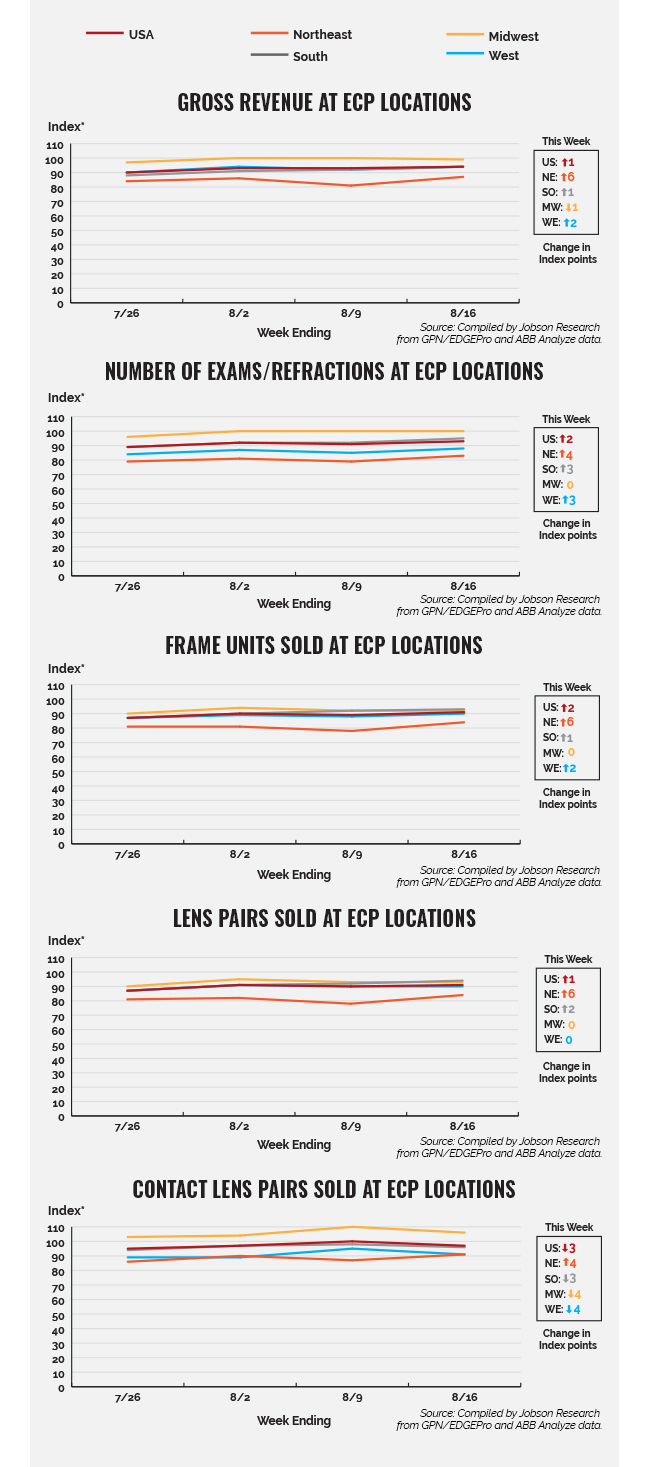

Regionally, optical sales fluctuated more widely than on a national level. The Northeast experienced the largest increases in sales this past week after lagging behind the other categories during previous weeks. Gross revenue, frame units and lens pairs grew by 6 index points in the Northeast. Even contact lens sales in the Northeast increased by 4 index points while all other regions experienced declines of either -3 or -4 index points for contact lenses. Most other regions were relatively flat for most categories, ranging mostly from 0 to 2 index points, with exams/refractions the slight standouts increasing by 3 index points in the South and the West.

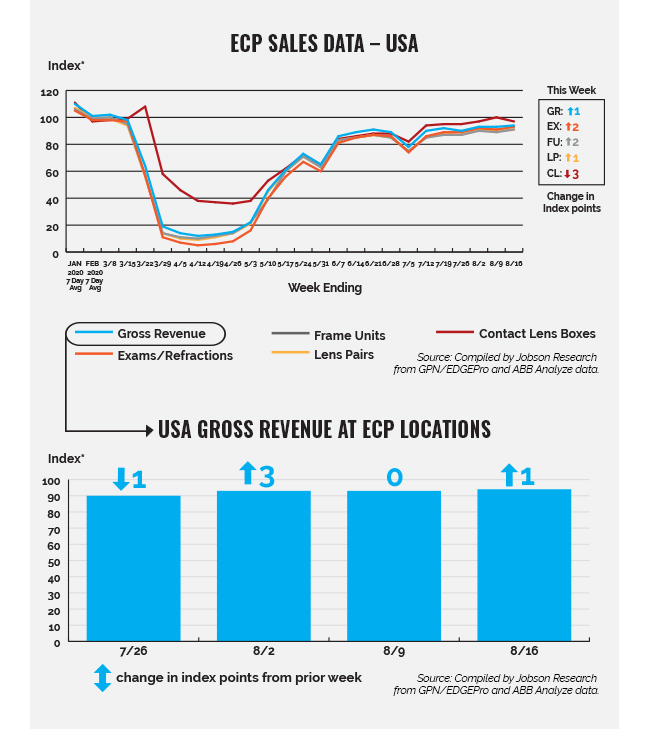

*The index baseline was developed by Jobson Research from total sales from an average seven days in the first quarter of 2019.This index baseline is equivalent to a score of 100. All other time periods going forward are calculated as a percent increase or decrease from the 100 baseline index of that period. This index is intended to show directional and magnitudinal change that the market is experiencing. Actual index scores are arbitrary meaning the baseline of 100 is simply used as a benchmark. Jobson Research shall not be held liable for any use or misuse of the data described and/or contained herein.

Please note that practices that use practice analytic systems tend to skew a bit larger and have higher revenue than practices that do not.

Source: GPN/EDGEPro and ABB Analyze contributed anonymous sales data used to determine gross revenue, exams/refractions, frame units, lens pairs, and contact lens boxes. Data was collected from approximately 3,500 independent eye care practices.

|