|

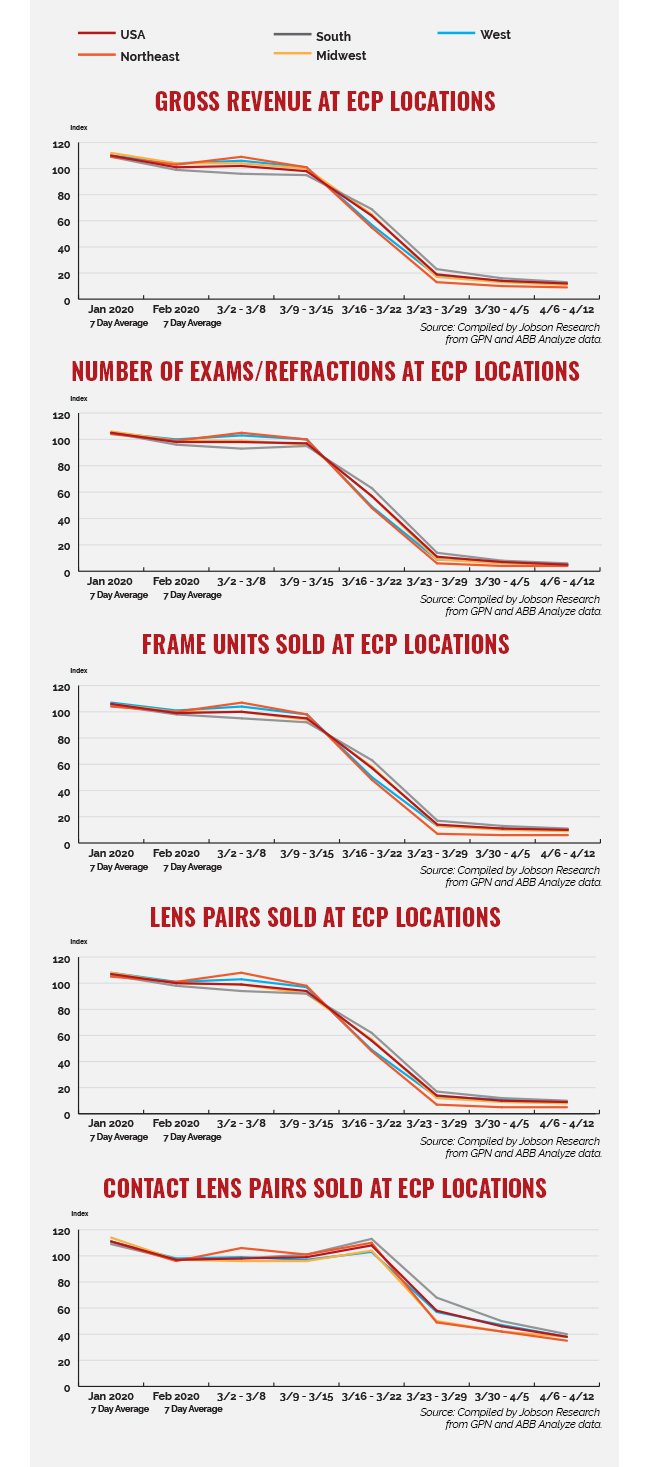

Nearly all product/service categories tracked are down both nationally and regionally. No categories, nationally or regionally, have shown an increase during the previous week. The only leveling off that has occurred is in the Northeast, which has maintained its index levels when comparing the week of April 6-12 with the previous week, March 30-April 5, for exams/refractions, frame units, and lens pairs. The rate of decline in all categories and regions has slowed when comparing the difference between the week of April 6-12 and the week of March 30-April 5 with the difference that occurred during the initial decline between the weeks of March 9-15 and March 16-22, except for contact lenses, which had its first major decline during the following week of March 23-29, and which has not fallen as far overall as the other product/service categories.

The index baseline was developed by Jobson Research from total sales from an average seven days in the first quarter of 2019. This index baseline is equivalent to a score of 100. All other time periods going forward are calculated as a percent increase or decrease from the 100 baseline index of that period. This index is intended to show directional and magnitudinal change that the market is experiencing. Actual index scores are arbitrary meaning the baseline of 100 is simply used as a benchmark. Jobson Research shall not be held liable for any use or misuse of the data described and/or contained herein.

Source: GPN and ABB Analyze contributed anonymous sales data used to determine gross revenue, exams/refractions, frame units, lens pairs, and contact lens boxes. Data was collected from approximately 3,500 independent eye care practices.

|