|

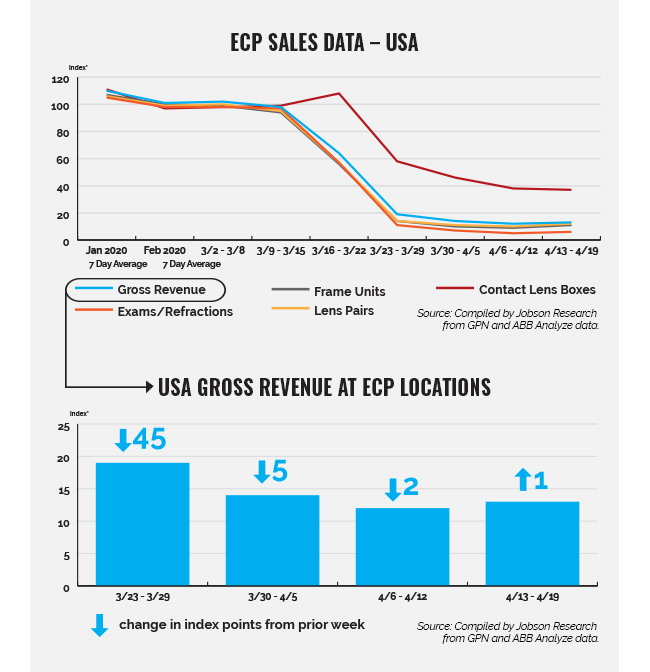

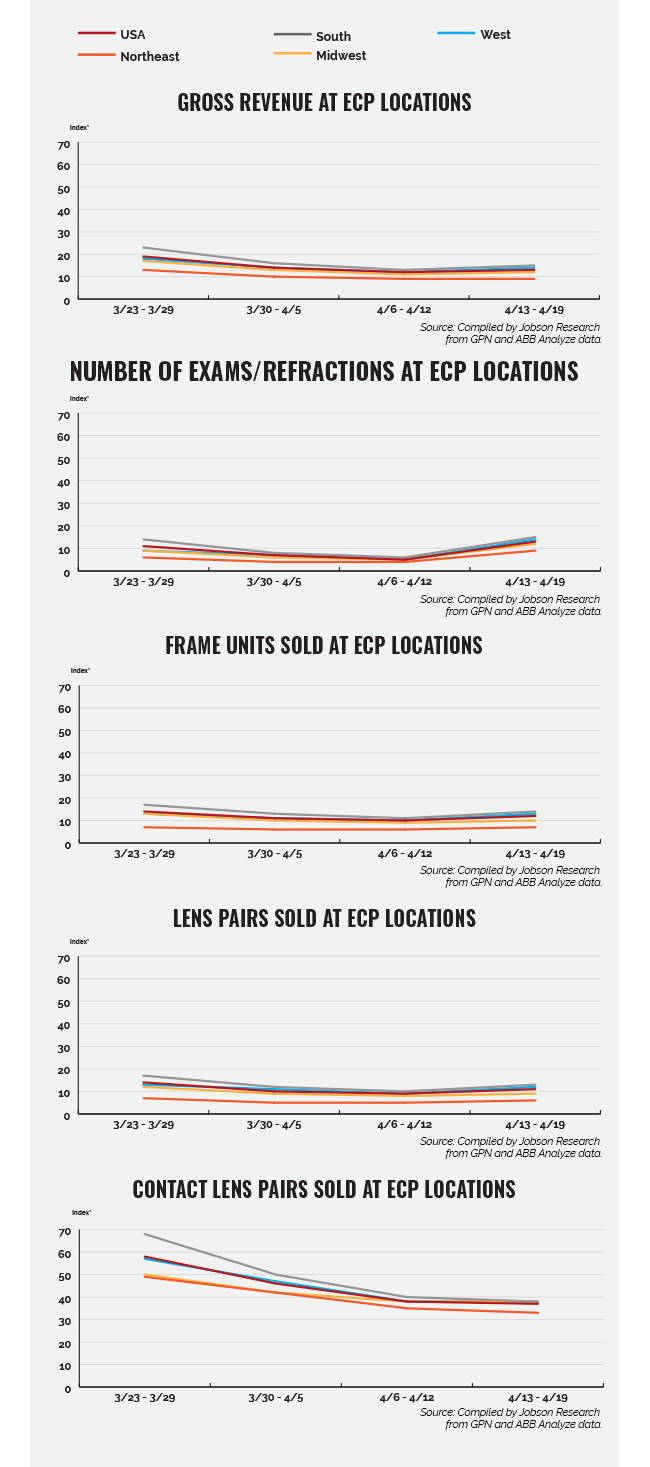

Most product/service categories being tracked in most regions throughout the United States also indicate a bottoming out and either a flattening or slight uptick in business. Other than contact lenses, which have been on a trajectory all their own since the beginning of this healthcare crisis, no product/service categories declined. The South and West were clearly regions with the largest upturn, although at rates of only 3 index points or less. Some were flat or up by a single index point. Those increasing more than just one index point were frame units and lens pairs in the South and West (up 3 index points) and gross revenue and exams/refractions in the South and West (up 2 index points). Remaining at a higher index level than all other categories, contact lens units stayed primarily flat at an index level of 38 in most regions, with slight declines in the Northeast and South.

* The index baseline was developed by Jobson Research from total sales from an average seven days in the first quarter of 2019. This index baseline is equivalent to a score of 100. All other time periods going forward are calculated as a percent increase or decrease from the 100 baseline index of that period. This index is intended to show directional and magnitudinal change that the market is experiencing. Actual index scores are arbitrary meaning the baseline of 100 is simply used as a benchmark. Jobson Research shall not be held liable for any use or misuse of the data described and/or contained herein.

Source: GPN and ABB Analyze contributed anonymous sales data used to determine gross revenue, exams/refractions, frame units, lens pairs, and contact lens boxes. Data was collected from approximately 3,500 independent eye care practices.

|